“Help! I have a ton of credit card debt. What do I do?”

“Help! I have a ton of credit card debt. What do I do?”

A buddy reached out to me earlier and was like, “Yo Chris! I remember you saying you had a bunch of debt and now you don’t. What do I do?” Well, since we’re all about shame-free financial education here, after chatting with them, I decided this is a great opportunity to discuss what to do with massive amounts of credit card debt.

Today, we’re going to discuss some strategies to get rid of credit card debt. We’ll talk about debt consolidation, debt relief, and some other strategies that you may not be aware of.

Real talk

I mentioned in my previous post that I’ll be as transparent with you all as possible. I’m not here to make you think that I’ve done anything magical, but I do know some things that may be able to help.

Fortunately, my credit was so bad that I didn’t have the opportunity to run up a ton of credit card debt. I probably would have if given the chance, so it’s good I wasn’t approved until I was able to trust myself with it. My debts were mainly bills that went to collections and some tax debt.

Being transparent, the majority of my debts were paid off from an inheritance I received when my grandfather passed away. It wasn’t a ton of money, but it was enough to get rid of most of those debts.

The other thing we need to discuss real quick is that credit cards are predatory in nature. They have ridiculous interest rates, and they’re banking on you not paying them back in a timely way. Eventually, I’ll teach you all some credit card strategies to make the credit cards work for you (and even how to get free stuff along the way). So make sure you’re subscribed so you don’t miss it.

The truth about eliminating credit card debt

On your road to getting your money right, the first thing you need to know is that there are a lot of scams out there. There are a ton of companies that do either illegal or borderline illegal things to get you to sign up with them. They’ll promise you the world and say they can eliminate your debt and all sorts of whacky stuff.

A good life philosophy is that if it sounds too good to be true, it probably is.

The only way to truly “eliminate” your credit card debt is by filing Chapter 7 bankruptcy, and this should always be a last resort. Bankruptcy stays on your credit report seven to 10 years. And the reason I put “eliminate” in quotes is because you’re most likely going to have to sell some of your stuff to repay your debts if you’re approved. Then, the bankruptcy wipes the rest away.

Typically, people only file bankruptcy if they’re in so much debt that the interest ensures that you’re probably never going to pay it off. This may not be as bad if you’re fairly young as well. I had a friend who got credit cards way too young, and she wasn’t responsible with them. She racked up 10s of thousands of dollars in credit card debt by her early 20s, so she filed for bankruptcy.

There are a lot more nuances to bankruptcy. If you want me to write a full post on it, let me know in the comments.

Does debt relief work?

Debt relief most likely isn’t what you think it is. These places may be able to help you with a strategy to take care of your debt, but they’ll charge you a fee.

I don’t know about you, but the reason I was in so much debt was because I was broke. Even today, I’m pretty frugal, so I try not to pay people for something I can do myself.

Debt relief companies often market themselves as experts in negotiating with your creditors and debt collectors. Trust me when I say that as long as you have a backbone, you can probably negotiate your debts yourself.

And if you don’t believe me that these places aren’t that great, you don’t have to. But the Consumer Financial Protection Bureau basically says the same thing.

“Debt relief or settlement companies are companies that say they can renegotiate, settle, or in some way change the terms of a person's debt to a creditor or debt collector. Dealing with these companies can be risky.”

There are some free places that offer debt counseling. They basically teach you some strategies and help you set up a plan to start taking care of your debt. Search for non-profit debt counseling places in your area if you’d like some face-to-face talk with someone who can educate you on your finances.

Alright, now that we’ve discussed some of the myths about taking care of your credit card debt, let’s discuss how to actually take care of it.

Debt consolidation is one of your best options

The problem with debt is that you’re usually paying multiple debts to different places, and each one has different interest rates. Not only is it hard to keep up with, but the interest can keep you in debt far longer than you think.

The benefit of debt consolidation is that you combine all your debt into one spot. If you can get a better interest rate, then you’re in a great position. There are a few ways to do this.

Before you do anything, calculate your total amount of debt so you know what you’re working with and what to apply for.

Debt consolidation loans

You can take out a debt consolidation personal loan and just pay off all of your debts. For example, let’s say you have 5 credit cards, each one has different interest rates, and you owe $15,000. In this scenario, you’re making 5 minimum payments, and it’s a hot mess.

Instead of doing that, you can take out a debt consolidation loan for $15,000, use that money to pay off all over your debts, and now you just pay back the one loan.

According to Bankrate, the average interest on debt consolidation loans are between 6 and 36 percent. 36 percent is insanely high, so you should probably only do this if you have a good enough credit score to get a low interest rate. Bankrate lists the best debt consolidation loans, so you can check out the interest rates, minimum score and max loan amounts.

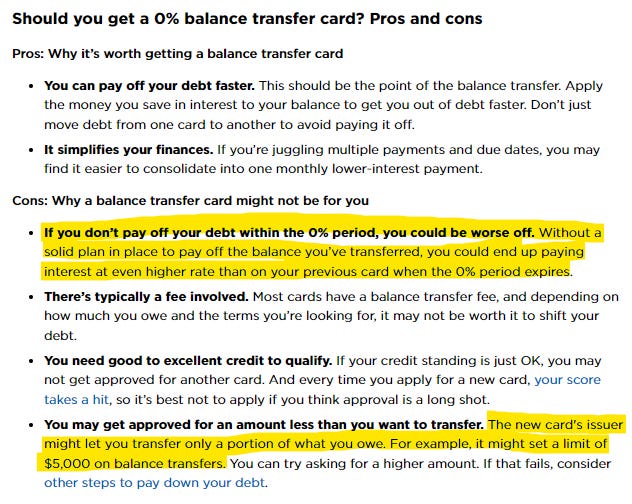

Balance transfer credit cards

Similar to debt consolidation personal loans, you can get a balance transfer credit card. It does exactly what it sounds like. You transfer the balances from your other cards to this one card, and you simplify everything.

Again, if you can get low interest rate, that’s great. These cards may also have fees though, so make sure you check.

I highly recommend that you check out this NerdWallet article with the best balance transfer credit cards. Most importantly, read the bottom section because it explains everything you need to know about how they work as well as the pros and cons.

HELOCs and 401(k) loans

These aren’t my specialty, but a HELOC is a Home Equity Line of Credit. Basically, if you own a home, you can take out a line of credit and use that money like a loan to pay off your debts.

Then, there are 401(k) loans. If you have a 401(k), you can borrow from it. I personally don’t like messing with my 401(k) because there are all sorts of weird tax rules, so I’d prefer not to unless I really needed to.

Other ways to pay off your credit card debt

To finish this off, I’m going to give you some other strategies to pay off your credit card debt without having to mess with any other companies or financial institutions. If you want me to do a deep dive into any of these methods, let me know in the comments.

Snowball method: There are a ton of debt strategies, but this is one of the most popular. Basically, you start saving and pay off your smallest balance in full. Then, you start saving and pay the next one off in full. You get some momentum and keep going. So, if your smallest credit card balance is $500, save up, pay that off. If the next one is $1,000, save up, pay that off, etc.

Sell your stuff: If you have stuff you don’t need, sell it. Hell, even if you think you “need” certain things, you probably don’t. It’s an easy way to make some extra cash. I’m not even in a ton of debt, but just today, I was looking at stuff I can sell to pay down some of my credit card balances.

Get a side hustle: There are an endless amount of side hustles. I personally have multiple side hustles like freelance writing, YouTube channel, and others. When that money comes in, I usually put it straight toward credit card debt.

If you want me to do a whole post with side hustle ideas, let me know in the comments. I know of a lot of them.

Get extra hours at work or negotiate a raise: I hope you’re seeing a pattern. Work with what you already have. If you’re in debt and a hard worker, it may be time to ask for a raise. If nothing else, see if you can pick up some extra shifts.

Settle your debt: When I paid off my collections, I settled almost all of my debts for less than what I owed. I’ve never settled a credit card debt, but I know with collections, you have a pretty good chance of paying less than you owe. Give it a try with your credit card company, and they may hook you up.

Ask a friend or family member for a loan: Yes, this sucks, but it’s better than every option I listed above. We all hate asking for money, but the benefit of this is that there’s no interest. Or, tell them you’ll pay them back 1-3% interest if you’d like. That’s probably way better than any personal loan or balance transfer card. I hate asking for money, but we gotta do what we gotta do.

And that’s it, these are some basic strategies for getting rid of your credit card debt.

As I mentioned multiple times in this post, let me know what else you want me to write about. I’m here to help you. If you have additional questions, leave comments. If you have questions, there’s a good chance other people do as well, so ask away.

I know it can seem like you’re never going to get out of debt, but I promise you that if you make a plan to start chipping away at it, you’ll be in a much better spot than you are now. You got this.