The simplest guide to credit scores you'll ever read

The simplest guide to credit scores you'll ever read

I’m proud of my 750 credit score, and when I say that I brought it up from the low 500s, the first question I get is, “How’d you do it?” I get this question more than any other finance question, so I wanted to put together a simple guide to help you understand what’s affecting your credit score.

As I mentioned in my welcome post, my credit was so bad that it was embarrassing. If you currently have or have ever had a low credit score, you know how much of a pain it can be. For most of my life, I didn’t mind that I couldn’t get credit cards or get approved to buy a car. The brutal part of it all was having to put down insane deposits whenever I signed a lease, started a phone contract, or turned on utilities.

My parents had terrible credit scores my entire life, so they weren’t able to teach me anything about credit. What’s crazy is that I’ve read a ton of personal finance books and barely any discuss credit. Maybe you’re in the same situation, so let’s start with the basics.

For the love of God, check your credit score

First off, if you don’t know your credit score, find out. I’ll eventually write a post about how many of us are terrified to check our finances, but you need to start ASAP if you aren’t. If you’re afraid to check your credit score or bank account, I get it. That’s how I lived most of my life, but that needs to change. You can’t fix what you don’t know about. Once I pulled the bandaid, it all became so much easier. I went from never checking to checking my accounts daily.

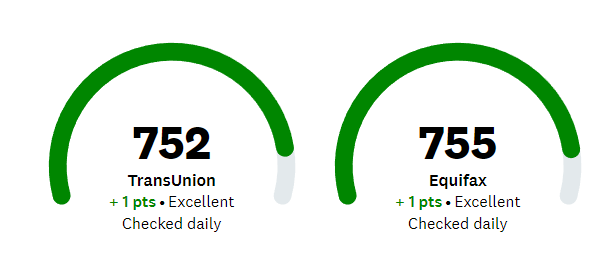

If you need to know your credit score, I personally use Credit Karma. It’s free and gives you scores from TransUnion and Equifax. It also has so many free features that I’m shocked they don’t charge for it.

If you want to check your credit report, you’re entitled to one free copy of it each year at AnnualCreditReport.com.

Credit terminology

When you’re learning about credit (or anything about finance), it can sound like a different language. Here are some of the primary terms you should know and brief explanations for each:

Credit score: A 3-digit number that basically tells businesses and financial institutions how much of a risk it is to give you money or something of value like a home to rent.

Credit report: This is a detailed look at your credit and shows everything affecting your score. I personally never check it, but you should if something seems weird about your credit score because sometimes there are errors or potential fraud.

Credit bureaus: When you pay or don’t pay bills, this is who that gets reported to, and they’re the ones making your score go up or down. The three primary ones are TransUnion, Equifax, and Experian. Then, there’s FICO.

Credit scoring models: This is how the bureaus score. Your score might be different at each credit bureau, but they should be fairly close. The three main bureaus use the VantageScore scoring model, but the main scoring model lenders look at is FICO. (I’ll explain these models below).

Credit inquiry: There are two types of inquiries: soft and hard. When someone checks your credit, it’s a hard or soft inquiry. A hard inquiry temporarily lowers your credit score. A soft inquiry does not.

Quick note, if you’re noticing that Credit Karma only shows two of your credit scores and I said your FICO score is a primary one, I appreciate that you’re paying attention. You can check your FICO score for free at myFICO.com. My bank and one of my credit cards provides my FICO score as part of being a member, so that’s where I check.

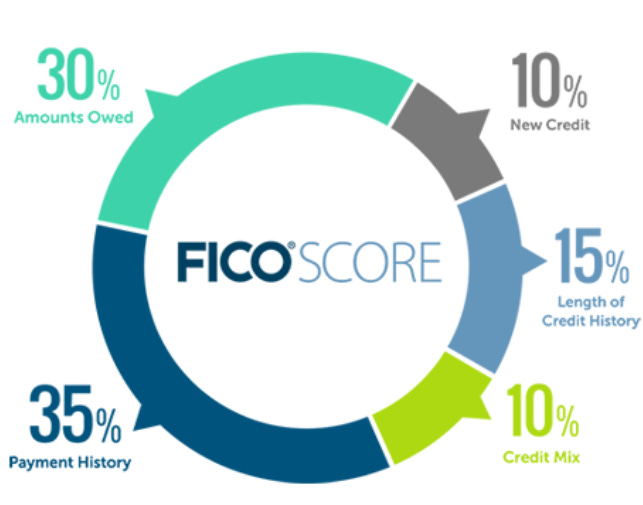

The 5 factors affecting your credit score

Here’s the meat and potatoes, ladies and gentlemen. These are the five factors affecting your score, and if you focus on these, you’ll be off to a great start. These are also credit terms, but they needed their own section.

First, you need to understand that credit scoring factors are “weighted”. This means some things are more important than others. Think of it like dating. How important are good looks versus personality? Maybe you’re someone who cares more about personality, so 70% of how you choose a partner is based on personality and 30% is looks. But then, there are those who don’t mind a terrible personality so their judgment is weighted 90% looks and 10% personality.

Back to credit talk. Here are the five primary factors and their weights based on the FICO scoring model:

Payment history (35%): How good you are at paying your bills on time

Credit utilization/amounts owed (30%): How much you owe compared to your max credit limit (I’ll explain this more. It’s semi-confusing.)

Length of credit history (15%): How long your credit accounts have been opened. The longer the better, so start getting lines of credit ASAP.

New credit (10%): How many new accounts you’ve opened (Opening multiple accounts in a short period of time can indicate you’re credit risk)

Credit mix (10%): Having experience with different types of credit (I’ll explain this one too)

Credit utilization

This needs a little more explaining. Aside from paying your bills on time, this is the most important thing, and it’s the difference between how much you owe versus your available credit. This is referred to as both your “credit utilization rate” and “credit utilization ratio”.

Ideally, you want your credit utilization as low as possible, but as long as it’s less than 30%, you should be fine. I personally try to keep mine around 10-15%.

So, how’s it calculated? Let’s say you have a $1,000 credit limit, and you’ve spent $500. $500 is 50% of $1,000, so your credit utilization is at 50%, which is no good. If you only spent $170 out of that $1,000 limit, your utilization is only 17%, which is great.

The credit bureaus are looking at your overall max credit limit. This means they’re adding the max limit of all of your credit cards to calculate this. I’ve had too many people think they’re looking at your individual cards, and that’s not really the case.

If you have a credit card with a $10,0000 credit limit and have only spent $1,000, and then you have a $2,000 credit card where you spent another $1,000, your utilization is only about 16%. How’d I get this number?

$10,000 + $2,000 = $12,000 (Overall max credit limit)

To find the percentage…I don’t know because I’m terrible at math. That’s why I use the Percentage Calculator website.

Credit mix

Don’t worry about this too much, especially if you’re just starting to build credit. There are two primary types of credit: revolving credit and installment credit. Having a good “credit mix” shows you can manage multiple types of credit.

Revolving credit is credit where you borrow, pay it back, and then you have access to that money again. The main form of revolving credit is credit cards. If you have a $1,000 limit and spend $800, you only have $200 left to spend. If you pay it off in full, you can then spend up to $1,000 again.

Installment credit is basically a loan. Car loans, home loans, student loans, and personal loans are all installment lines of credit. You’re loaned a certain amount, and as you pay it off, the total amount goes down.

I only have credit cards and a car loan, and my credit mix is fine. You don’t need much to earn this one.

Transparency

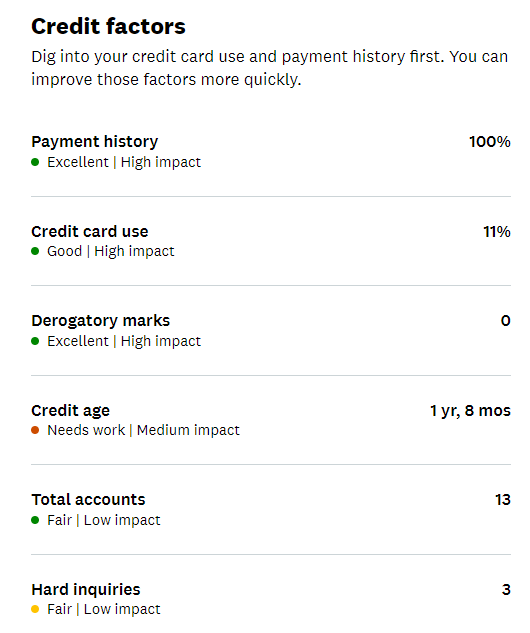

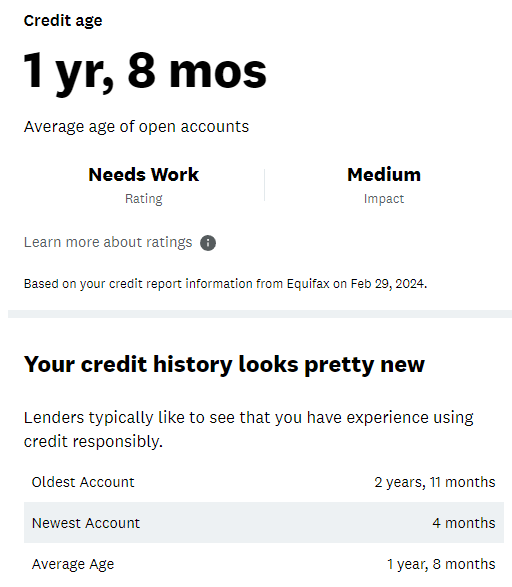

I’m going to be as transparent as I think is necessary with you all. Since we’re talking about finances here, I may not show you everything, but I’ll show you a lot. Here’s what my credit factors look like. And all of this information is free over at Credit Karma (They’re not a sponsor, but they really should be. Holler at me if you’re reading this, Credit Karma).

I’ll be honest, I think the credit age one is bugged because it’s said that for the last few years. What’s cool is that you can click on each of these factors for a more detailed look.

See, this is incorrect. My oldest account is older than 2 years and 11 months. If I cared enough, I could make some calls and fill out some forms, but my credit score is doing great. So, I’m not too worried about it.

Your credit isn’t being affected the way you think

Some things improve your credit and others don’t. Some of the things that don’t improve your credit can hurt your credit, and this is important to understand. I just wanted to throw this out there because I didn’t learn this until later in life. Maybe you already knew that, but this is a shame-free environment, baby! So here’s the low down for those of you who didn’t know.

Only certain things are reported to the credit bureaus. Here’s what’s not getting reported, which is pretty annoying, but it’s just how it is:

Making rent payments

Making utility payments

Making phone bill payments

I know. It sucks, right? There are some services out there that will report some of these extra things to boost your score slightly. I personally use ExperianBoost. It’s free, but they’ll try to get you to sign up for add-ons, but you don’t need to. This lets you add your phone bill as well as streaming services and some other stuff, but it only improves your score with Experian.

Now, even though these places aren’t reporting to the credit bureaus to help improve your credit when you make your payments, they can hurt your credit if you don’t pay. I’m not joking when I say I was a financial mess. I didn’t pay many bills and just figured they’d go away. Nope! If you don’t pay, they send it to collections, which can lower your score. So, pay your bills.

Final thoughts

This had a lot of information, but it’s probably the simplest way I could pack in all of the primary information. But for those of you who had no or very little knowledge about credit, I hope it brought you some value.

Now, if you’re someone like me, you might be pretty annoyed because I didn’t discuss how to fix your credit or what to do if you don’t have any credit. If you’re one of these people leave a comment so I know what topics to cover in the future. Let me know what’s most important to you and what you’re struggling with.

This is my first post, so help me help you. If you want to learn more about credit, let me know. If you’re more interested in learning how to invest, budget, save, get out of debt, or whatever, let me know.

And be sure to subscribe so you don’t miss any upcoming posts. I’ll see you in the next one!

Lastly, if you found any of this information valuable please share it so we can help more people get their money right.